A House Used to Cost 3 Years of Your Salary. Now It's 5. What Happened?

I'm not an economist. I'm not a policy analyst. I'm a guy who served in the military, went to culinary school, worked hard, and still can't afford a house. And I'm starting to wonder if the math ever actually worked — or if I just missed the window.

So I did what any frustrated person does at 2am. I pulled the numbers. Median household income vs. median home prices across four snapshots in time. What I found made me angry. Then it made me sad. Then it made me want to show everyone I know.

Let me walk you through it.

The Four Snapshots

I picked four moments that tell the story of housing in America over the last two decades:

- Pre-2008 Crash (2006) — the height of the housing bubble, right before everything fell apart.

- Post-2008 Crash (2010) — the aftermath, when home prices bottomed out.

- Pre-Pandemic (2019) — the last "normal" year before COVID changed everything.

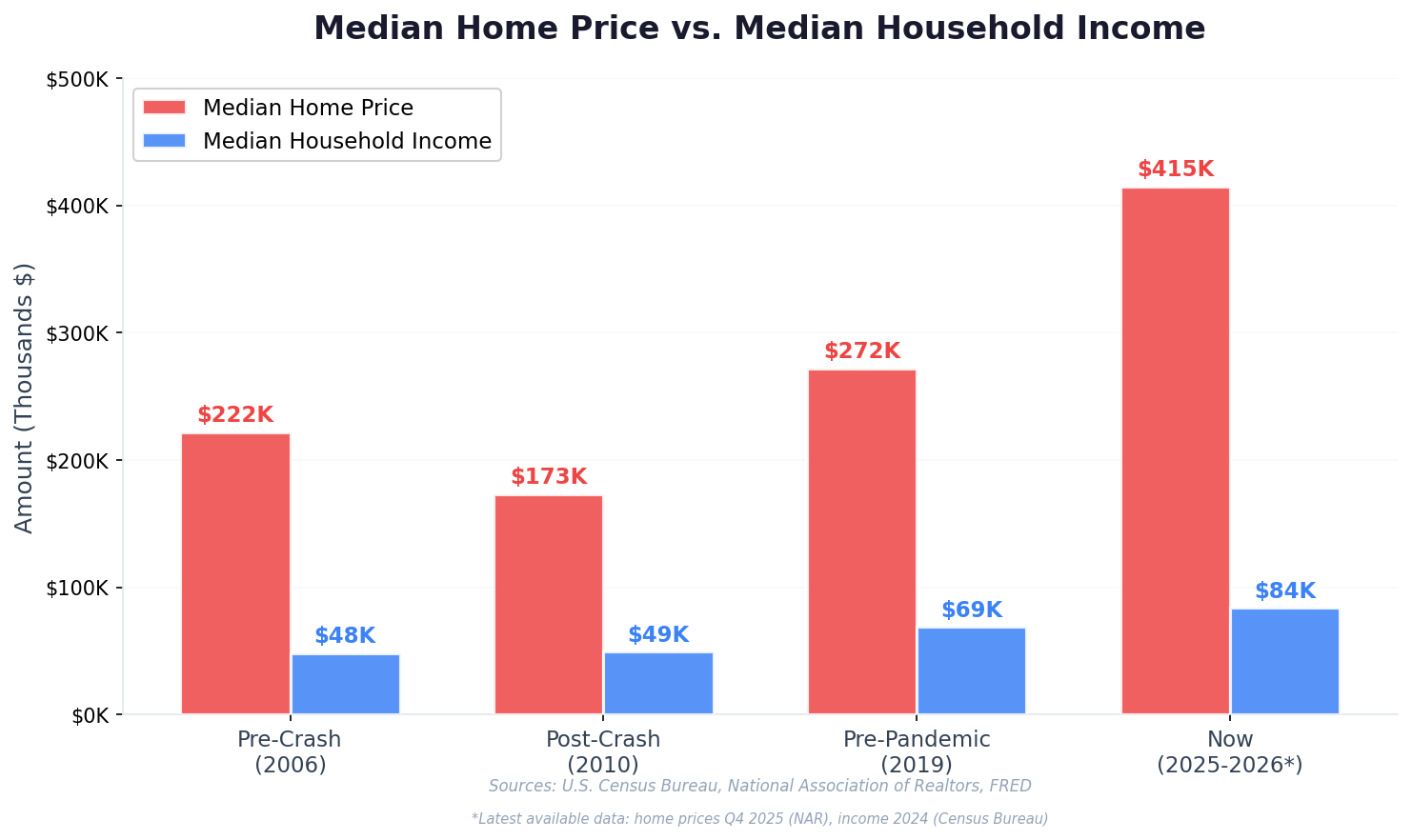

- Today (2025-2026) — where we currently stand, using the latest available data. Home prices are from Q4 2025 via the National Association of Realtors. Income data is from the 2024 Census Bureau report, which is the most recent the government has published.

Here's what the raw numbers look like:

In 2006, the median existing home in America cost about $222,000 and the median household was pulling in roughly $48,200 a year (U.S. Census Bureau, National Association of Realtors). Not great, but people were buying.

By 2010, after the crash wiped out trillions in housing wealth, that median home dropped to around $173,000. Incomes barely moved — $49,300 (Census Bureau). Painful for people who bought at the top, but suddenly the math worked for new buyers again.

Fast forward to 2019. Homes crept back up to $272,000 while incomes had grown to $68,700 (Census Bureau, NAR). Things felt tight, but not impossible.

And now? The median existing home costs $414,900 as of late 2025 (National Association of Realtors). Median household income is about $83,700 based on the latest Census data (Census Bureau, "Income in the United States: 2024"). Incomes went up, sure. But home prices jumped 53 percent since 2019 while incomes grew by about 22 percent (Harvard Joint Center for Housing Studies). That gap isn't closing. It's accelerating.

The Ratio That Tells the Real Story

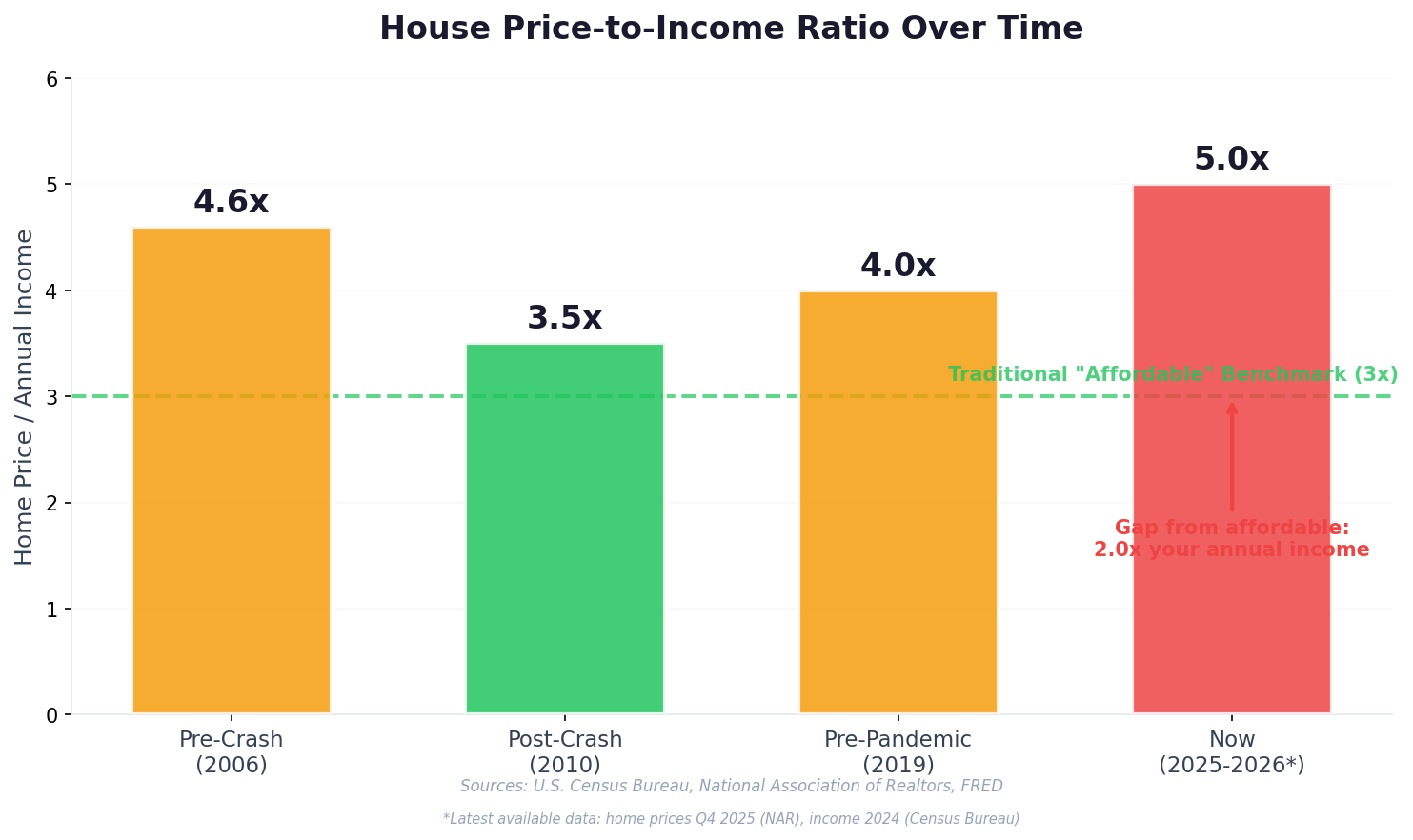

There's an old rule of thumb in personal finance: a house should cost about three times your annual household income. That's the benchmark financial advisors have used for decades. Three times your salary. That's supposed to be "affordable."

Here's where each of those four time periods lands on that ratio:

Pre-Crash (2006): 4.6x your income

Post-Crash (2010): 3.5x your income

Pre-Pandemic (2019): 4.0x your income

Today (2025-2026): 5.0x your income

Look at 2010. After the worst financial crisis most of us had ever seen, after the housing market collapsed, after millions lost their homes — that was the closest we've been to "affordable" in the last twenty years. 3.5x. Still above the 3x benchmark, but at least in the neighborhood.

And now? We're at 5.0x. That's not in the neighborhood. That's not even in the same zip code.

To put it differently: if you earn the median household income of $83,700, the traditional 3x rule says you should be able to buy a home for about $251,000. The actual median home price is $415,000. That's a gap of $164,000. Almost two full years of your gross salary — before taxes, before food, before gas, before anything.

And here's the kicker — even if you found a home at that $415,000 median price, most lenders won't even approve you unless you're making at least $100,000 to $110,000 a year (Redfin, LoanPronto, based on current 6-7% mortgage rates and a 43% debt-to-income ratio). The median household income is $83,700. Do the math. The average American family doesn't even qualify for the average American home.

What This Feels Like on the Ground

I know these are just numbers on a page. But let me make it personal.

I went to culinary school. I followed the "follow your passion" advice that everyone loves to give. I built a solid career. A chef making $75,000 a year sounds like they should be doing fine, right? That's above median income.

Run the math. At 3x, I could afford a $225,000 house. Find me that house in any major metro where the restaurant jobs actually are. You can't. At today's 5.0x ratio, the "expected" home price for someone at my income level is about $375,000. And the actual median is still $415,000 — meaning even by today's stretched standards, it's out of reach. And at $75,000, I probably wouldn't even get approved for a $400,000 mortgage.

I did the military thing. I did the education thing. I did everything they tell you to do. And the gap just keeps getting wider.

Why This Matters Beyond Home Buying

This isn't just about whether you can buy a house. When housing eats up this much of the economy, it ripples through everything.

People delay starting families. They stay in jobs they hate because they can't afford the risk of changing careers. They can't save for retirement because rent takes 30 to 40 percent of their take-home pay. They can't invest, can't take risks, can't build the kind of generational wealth that previous generations took for granted.

I was listening to the Impact Theory podcast a while back, and the host was making the argument that minimum wage doesn't need to be raised because minimum wage was never meant to be a permanent thing. It's supposed to be a stepping stone. And sure, I get the logic on paper. But then I started thinking about all the people I actually know in real life who are going to be earning minimum wage or close to it for the foreseeable future. Not because they're lazy. Not because they don't work hard. They just don't have the skills to move into management, or they don't want to be managers — and there's nothing wrong with that.

But does that automatically mean those people don't deserve to buy a house? Does it mean they don't deserve to feel like they can afford to start a family? Just because someone isn't a high earner or a type-A go-getter or a startup founder doesn't mean they shouldn't have the ability to build a stable life. The economy should work for regular people, not just the ones who claw their way to the top.

The Census Bureau reported that median household income grew about 22 percent between 2019 and 2024 (Census Bureau, "Income in the United States: 2024"). Sounds decent until you realize home prices grew 53 percent in the same period — more than double the rate of income growth (Harvard Joint Center for Housing Studies).

And here's what really gets me: the official economic indicators keep saying things are fine. GDP is up. Unemployment is low. The stock market is doing great if you own stocks. But for regular working people trying to buy their first home? The numbers tell a completely different story.

I'm Not Claiming to Have the Answers

I want to be upfront about that. I don't know how to fix housing affordability. I don't know if it's a supply problem, a demand problem, a policy problem, or all three. Smarter people than me are working on it — or at least I hope they are.

What I do know is that the math doesn't lie. The house-price-to-income ratio is the highest it's been in at least two decades — higher than the peak of the 2006 housing bubble (FRED, St. Louis Fed). And unlike 2006, this time it's not being driven by subprime lending and speculation — it's just the raw cost of housing outpacing what people earn.

I built TrustHub because AI tools gave me hope that I could create something, build value, and maybe — finally — close that gap for myself. Not everyone has that option. Not everyone wants to learn to code or build a startup. And they shouldn't have to. A teacher, a chef, a mechanic — these people should be able to afford a home.

That used to be the deal. Work hard, play by the rules, buy a house. Somewhere along the way, the deal changed. And nobody told us.

What's your experience? Are you feeling this gap? Have you given up on homeownership, or are you still trying to make the math work? I want to hear from people who agree and disagree. Drop a comment.

Data sources: U.S. Census Bureau — "Income in the United States: 2024" (median household income), National Association of Realtors via FRED/St. Louis Fed (median existing home sale prices), Harvard Joint Center for Housing Studies (price-to-income trends).

0 Comments

No comments yet. Be the first to reply!